How to Purchase Reverse Mortgage and Use It to Fund Your Future

How to Purchase Reverse Mortgage and Use It to Fund Your Future

Blog Article

Unlock Financial Liberty: Your Overview to Acquiring a Reverse Mortgage

Recognizing the ins and outs of reverse mortgages is essential for home owners aged 62 and older seeking monetary liberty. As you consider this option, it is essential to comprehend not just just how it functions however likewise the effects it may have on your monetary future.

What Is a Reverse Home Mortgage?

The fundamental appeal of a reverse home loan depends on its potential to enhance economic versatility during retired life. Home owners can use the funds for various purposes, consisting of clinical expenses, home enhancements, or daily living prices, hence offering a security internet throughout a critical point of life.

It is necessary to recognize that while a reverse home mortgage enables for increased capital, it also reduces the equity in the home over time. As interest accumulates on the superior financing balance, it is vital for prospective borrowers to very carefully consider their long-lasting monetary plans. Consulting with a monetary expert or a reverse home mortgage professional can offer beneficial insights right into whether this alternative straightens with an individual's monetary goals and situations.

Qualification Requirements

Understanding the qualification requirements for a reverse mortgage is important for property owners considering this financial choice. To qualify, applicants should go to least 62 years of ages, as this age requirement allows seniors to accessibility home equity without monthly home loan payments. In addition, the home owner has to occupy the house as their primary house, which can consist of single-family homes, particular condos, and produced homes fulfilling specific guidelines.

Equity in the home is one more vital requirement; home owners normally need to have a substantial amount of equity, which can be determined via an assessment. The quantity of equity offered will directly influence the reverse home mortgage quantity. Candidates must demonstrate the capability to maintain the home, consisting of covering building taxes, home owners insurance, and upkeep expenses, ensuring the residential or commercial property continues to be in great condition.

Additionally, prospective customers must go through an economic evaluation to review their earnings, credit rating, and overall economic scenario. This evaluation assists lenders determine the applicant's capacity to meet recurring responsibilities associated to the building. Satisfying these demands is critical for protecting a reverse home mortgage and making certain a smooth monetary change.

Advantages of Reverse Mortgages

Countless benefits make reverse mortgages an appealing choice for senior citizens wanting to enhance their financial adaptability. purchase reverse mortgage. Among the primary advantages is the ability to transform home equity into cash money without the requirement for monthly home loan settlements. This attribute allows seniors to access funds for different requirements, such as clinical costs, home improvements, or daily living costs, consequently alleviating monetary anxiety

Furthermore, reverse home loans give a safeguard; seniors can remain to live in their homes for as lengthy as they meet the loan requirements, fostering stability during retired life. The profits from a reverse home mortgage can additionally be made use of to postpone Social Security advantages, possibly resulting in greater payouts later on.

Additionally, reverse mortgages are non-recourse finances, suggesting that debtors will certainly never owe greater than the home's value at the time of sale, shielding them and their heirs from monetary responsibility. The funds obtained from a reverse home loan are normally tax-free, including another layer of monetary alleviation. Generally, these advantages position reverse home mortgages as a useful option for seniors seeking to improve their monetary circumstance while preserving their treasured home environment.

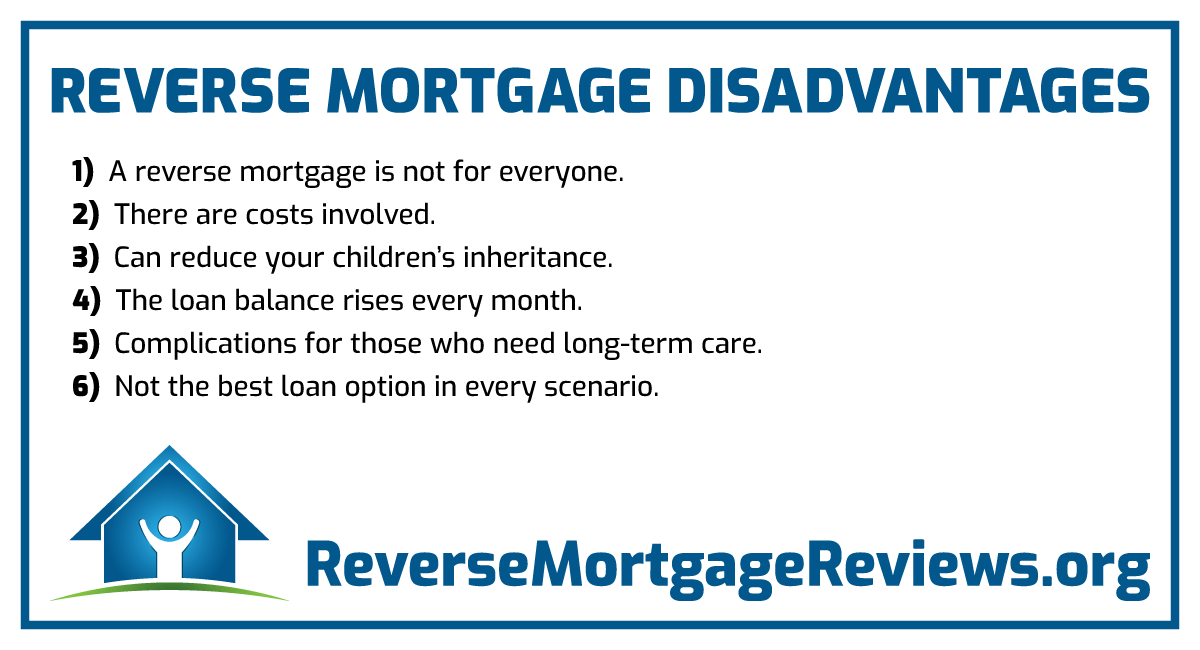

Fees and prices Entailed

When taking into consideration a reverse home loan, it's necessary to know the different costs and charges that can affect the overall monetary image. Understanding these expenses is critical for making an informed choice about whether this economic product is best for you.

One of the main expenses use this link connected with a reverse mortgage is my latest blog post the source fee, which can vary by loan provider however usually varies from 0.5% to 2% of the home's assessed value. Furthermore, house owners ought to expect closing prices, which might consist of title insurance coverage, evaluation charges, and credit record fees, typically amounting to a number of thousand dollars.

Another considerable expense is home loan insurance policy costs (MIP), which protect the loan provider against losses. This fee is typically 2% of the home's worth at closing, with a recurring annual premium of 0.5% of the remaining loan equilibrium.

Last but not least, it is necessary to take into consideration ongoing prices, such as real estate tax, home owner's insurance, and upkeep, as the customer continues to be responsible for these expenses. By thoroughly evaluating these fees and prices, house owners can much better evaluate the economic ramifications of pursuing a reverse home loan.

Actions to Begin

Getting going with a reverse home loan includes several vital steps that can help streamline the process and guarantee you make notified choices. Examine your financial scenario and identify if a reverse home loan aligns with your long-lasting goals. This consists of reviewing your home equity, existing debts, and the necessity for added revenue.

Following, study numerous loan providers and their offerings. Seek respectable organizations with positive evaluations, clear charge frameworks, and affordable rates of interest. It's vital to compare terms and problems to find the ideal suitable for your needs.

After selecting a loan provider, you'll require to complete a comprehensive application procedure, which typically requires paperwork of income, assets, and property information. Take part in a counseling session with a HUD-approved counselor, that will certainly offer understandings into the implications and duties of click resources a reverse home mortgage.

Verdict

In conclusion, reverse home mortgages present a viable option for seniors looking for to improve their financial security during retirement. By converting home equity right into accessible funds, property owners aged 62 and older can address various economic demands without the stress of regular monthly payments.

Understanding the intricacies of reverse home mortgages is important for property owners aged 62 and older looking for economic flexibility.A reverse home loan is an economic product made primarily for property owners aged 62 and older, permitting them to convert a section of their home equity into cash money - purchase reverse mortgage. Consulting with a reverse home mortgage or an economic consultant expert can supply important insights into whether this choice lines up with a person's monetary goals and conditions

Additionally, reverse home loans are non-recourse car loans, implying that consumers will never owe even more than the home's value at the time of sale, safeguarding them and their successors from monetary obligation. Overall, these advantages position reverse home loans as a practical remedy for elders seeking to boost their monetary scenario while maintaining their treasured home environment.

Report this page